What is Fama-French data?

The Fama French 3-factor model is an asset pricing model that expands on the capital asset pricing model by adding size risk and value risk factors to the market risk factors. The model was developed by Nobel laureates Eugene Fama and his colleague Kenneth French in the 1990s.

Where can I get Fama-French data?

The Fama-French data source is Kenneth French’s web site at Dartmouth. The Pastor-Stambaugh Liquidity series are described by L.

What are the Fama and French five factors?

Taking inspiration from the Fama French five-factor model, we can develop a multi-factor stock selection strategy that focuses on five factors: size, value, quality, profitability, and investment pattern. First, we run a Coarse Selection to drop equities which have no fundamental data or have too low prices.

How are the Fama French factors created?

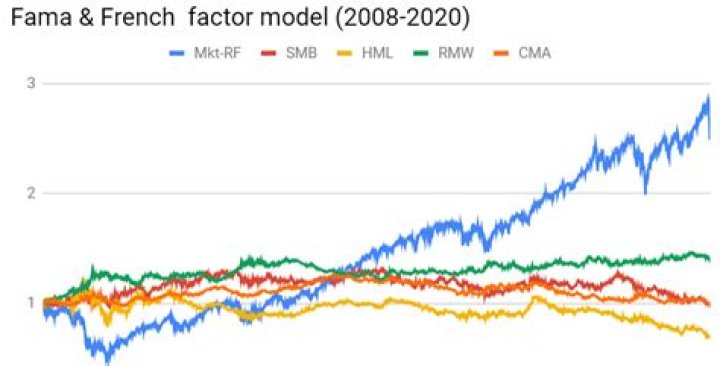

The Fama/French factors are constructed using the 6 value-weight portfolios formed on size and book-to-market. (See the description of the 6 size/book-to-market portfolios.) – 1/3 (Big Value + Big Neutral + Big Growth). – 1/2 (Small Growth + Big Growth).

Why is Fama French better than CAPM?

CAPM has been prevalently used by practitioners for calculating required rate of return despite having drawbacks. It means that Fama French model is better predicting variation in excess return over Rf than CAPM for all the five companies of the Cement industry over the period of ten years.

How are Fama French factors constructed?

The Fama/French 5 factors (2×3) are constructed using the 6 value-weight portfolios formed on size and book-to-market, the 6 value-weight portfolios formed on size and operating profitability, and the 6 value-weight portfolios formed on size and investment.

How do you make a Fama French portfolio?

The Fama-French Portfolios are constructed from the intersections of two portfolios formed on size, as measured by market equity (ME), and three portfolios using the ratio of book equity to market equity (BE/ME) as a proxy for value.

Why Fama French model is important?

Importance of the Fama-French Three-factor Model CAPM formula shows the return of a security is equal to the risk-free return plus a risk premium, based on the beta of that security. The studies conducted by Fama and French revealed that the model could explain more than 90% of diversified portfolios’ returns.

Is Fama French model better than CAPM?